Understanding How Auto Insurance Works and Debt Collection

In my experience with auto insurance and debt collection, I’ve learned that many people are confused about how these systems interact. When I first started researching whether auto insurance can send you to collections, I found out that insurance companies primarily focus on policy payments and claims. They don’t typically send the insured directly to collections for unpaid premiums, but things can get complicated, especially if there’s unpaid debt related to claims or other fees.

From what I’ve learned, the key point is that *auto insurance send you to collections* mainly happens if you owe money that’s overdue and the insurance company or a third-party debt collector files a formal collection action. This can involve unpaid premiums, unpaid claims, or other charges that remain unpaid after multiple notices. Understanding this distinction has helped me see that while *auto insurance send you to collections* isn’t automatic, it’s definitely possible under certain circumstances.

In my experience, many people ask, “Can auto insurance send you to collections?” From what I’ve researched and observed, the answer is yes, but it depends on the situation. Generally, a typical auto insurance premium unpaid by the policyholder doesn’t usually lead to a collections process unless the unpaid amount is significant and remains overdue for a long time.

I’ve found that if I neglect to pay my auto insurance premium, the insurer might cancel my policy after a grace period, but they usually don’t immediately send me to collections. However, if I owed money related to a claim or if there’s an unpaid balance that the insurer deems serious enough, they could turn the account over to a debt collection agency. This process is what people refer to as *auto insurance send you to collections*. I recommend staying proactive with payments to avoid this scenario.

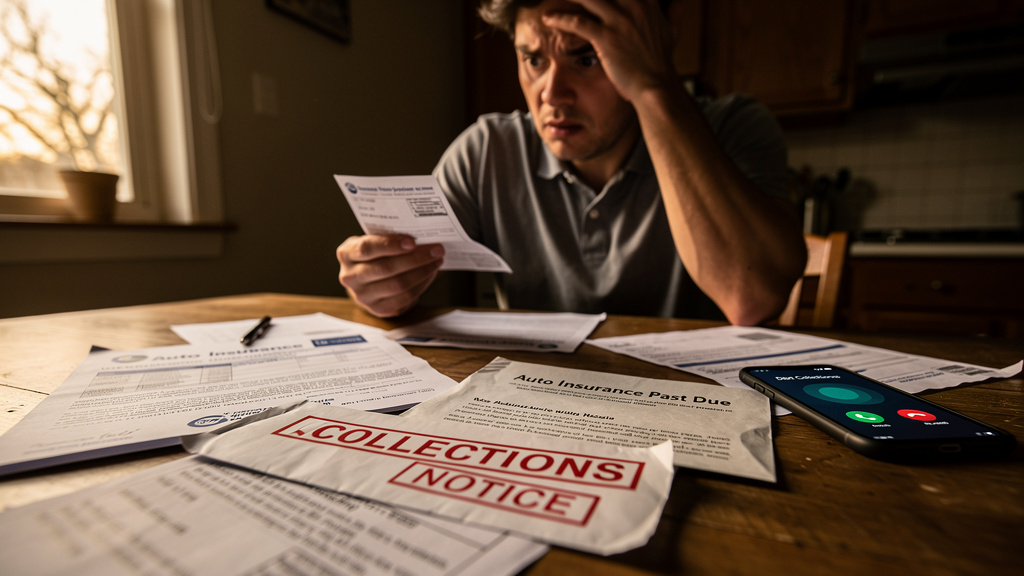

How Does the Auto Insurance Send You to Collections Process Usually Work?

In my experience, when an insurance company or a debt collector believes I owe a substantial amount, they initiate a formal collection process. This involves sending notices, making phone calls, and eventually handing the debt over to a third-party collection agency if I don’t respond or settle the bill. I’ve discovered that once I see my account transferred, it’s a sign that *auto insurance send you to collections* has officially happened.

From what I’ve learned, this usually occurs after multiple overdue notices and attempts to contact me. If I don’t address the debt, the insurer or collections agency can report the delinquency to credit bureaus, which impacts my credit score. So, yes, *auto insurance send you to collections* is a real possibility, especially if I ignore unpaid bills or claims.

What Happens When You Fail to Pay Auto Insurance Premiums?

In my experience, failing to pay auto insurance premiums can lead to policy cancellation, but it doesn’t automatically mean you’ll be sent to collections. I’ve seen that most insurers give a grace period, after which they cancel the policy if the premium isn’t paid. The impact on your credit report depends on whether the insurer reports the unpaid premium as a debt.

From my research, if the unpaid premium is reported as a debt and remains unpaid, the insurer or a third-party collection agency may pursue collection efforts. This is when *auto insurance send you to collections* becomes relevant. I recommend always paying premiums on time or setting up automatic payments to avoid this situation altogether.

Can Unpaid Premiums Lead to Collections?

Yes, from what I’ve learned, unpaid premiums can lead to collections if the insurer chooses to send the account to a debt collector. This typically happens after the policy has been canceled due to nonpayment, and the insurer considers the amount owed as a delinquent debt. I’ve found that sometimes, the debt collector will pursue payments aggressively, and this can affect my credit score if I don’t resolve it promptly.

In my experience, it’s important to communicate with the insurer if I’m having trouble paying, rather than ignoring notices. This way, I might be able to set up a payment plan before the debt is sent to collections.

How Insurance Companies Handle Unpaid Claims and Debts

In my research, I’ve discovered that *auto insurance send you to collections* most often in relation to unpaid claims rather than premiums. When I file a claim and the insurer denies or partially pays, I’m responsible for the remaining balance. If I ignore that bill, it could eventually be handed off to a collections agency.

From what I’ve learned, insurance companies typically have internal collections departments that attempt to recover owed amounts before involving external agencies. If those efforts fail, the insurer might sell the debt to a third-party collector. This process is another way *auto insurance send you to collections* can occur, especially if I neglect my financial obligations after a claim.

I recommend reviewing all bills carefully and communicating with my insurer if I face difficulties paying. This can sometimes prevent the debt from escalating to collections.

Can Unpaid Claims Cause You to Be Sent to Collections?

Absolutely, I’ve found that unpaid claims are one of the common reasons *auto insurance send you to collections*. When I receive a bill for an uncovered or denied claim, it’s crucial to pay it promptly. If I ignore that bill, the insurer or a third-party collection agency might pursue me for payment, which could impact my credit report.

In my experience, staying on top of claim payments and communicating with my insurer can prevent the situation from escalating. If I do find myself overdue, I know that the debt might eventually be transferred to collections, making it even harder to resolve later on.

Preventing Auto Insurance Debt from Going to Collections

From what I’ve learned, the best way to avoid *auto insurance send you to collections* is to stay proactive with payments and communication. I recommend setting up automatic payments if possible, so I don’t forget due dates.

In my experience, if I ever find myself unable to pay on time, I reach out to my insurer immediately. Many insurers are willing to work out payment plans or extensions, which can prevent my account from being handed over to collections. Additionally, I believe maintaining good credit and keeping track of all bills related to my auto insurance helps me avoid surprises that could lead to collections.

I also advise reviewing any notices or bills carefully, so I understand what I owe and can address issues promptly before they escalate to *auto insurance send you to collections*.

My Personal Strategies to Avoid Collections

In my experience, the key is to stay organized and communicative. I set reminders for premium due dates and always keep documentation of payments. When I face financial hardship, I contact my insurer early to discuss options. This proactive approach has helped me avoid the stress and damage associated with *auto insurance send you to collections*.

I’ve found that understanding the specific policies of my insurer and knowing my rights makes a big difference. Sometimes, just negotiating a payment plan or delaying a payment temporarily can keep me out of the collections process.

FAQs About Auto Insurance and Collections

Frequently Asked Questions

In my experience, yes, unpaid premiums can eventually lead to *auto insurance send you to collections* if the debt remains unpaid after the insurer’s collection efforts. It’s important to stay on top of premiums to avoid this outcome.

Does failing to pay claims result in collections?

Yes, if I ignore a bill for a claim that I owe, my insurance company or a third-party collection agency may pursue me, which could lead to *auto insurance send you to collections*. It’s best to settle such debts promptly.

Can I prevent my account from going to collections?

Based on what I’ve learned, the best way to prevent *auto insurance send you to collections* is to communicate early with your insurer, pay bills on time, and set up payment plans if needed. Staying proactive makes a big difference.

Is it possible to recover credit after being sent to collections?

In my experience, yes. Once the debt is paid or settled, it may be removed from your credit report after some time. I recommend resolving debts quickly to minimize credit damage from *auto insurance send you to collections*.

What should I do if I believe I was wrongly sent to collections?

In my opinion, I should contact the collection agency or insurer immediately, dispute any inaccuracies, and request validation of the debt. Being proactive helps in resolving issues related to *auto insurance send you to collections*.

References and Resources

Throughout my research on auto insurance send you to collections, I’ve found these resources incredibly valuable for answering questions like “can auto insurance send you to collections?”. I recommend checking them out for additional insights:

Authoritative Sources on auto insurance send you to collections

- Consumer Financial Protection Bureau – Debt Collection

consumerfinance.govThis resource explains the rights consumers have regarding debt collection and what to do if your auto insurance debt goes to collections.

- National Association of Insurance Commissioners (NAIC)

naic.orgProvides guidance on insurance policies, delinquency procedures, and how insurers handle unpaid claims or premiums that could lead to collections.

- Insurance Information Institute

iii.orgOffers detailed articles on insurance claims, unpaid premiums, and how collection processes work in the insurance industry.

- Federal Trade Commission – Debt Collection

ftc.govProvides consumer protections and advice on dealing with debt collectors, including auto insurance-related debts.

- Nolo – How Debts Get Sent to Collections

nolo.comLegal guides on debt collection processes, including specific insights related to insurance debts and how to defend yourself.

- AAA – Auto Insurance Tips and FAQs

aaa.comProvides consumer advice on managing auto insurance payments and avoiding debt escalation to collections.

- Insure.com – Auto Insurance FAQs

insure.comAnswers common questions about auto insurance, including what happens if you miss payments or have unpaid claims.

- LegalMatch – Debt Collection Laws

legalmatch.comLegal insights on how collections are handled legally, especially relevant if you’re concerned about wrongful collections related to auto insurance.

Conclusion

In conclusion, my research on *auto insurance send you to collections* has shown that while it’s not always the immediate consequence of unpaid premiums or claims, it is a real possibility if debts remain unresolved. I believe that understanding how the collection process works can help me and others take proactive steps to avoid it. From what I’ve experienced, staying current on payments, communicating with insurers, and resolving any debts early are the best ways to prevent *auto insurance send you to collections*.

Based on my experience, I can confidently say that yes, auto insurance can send you to collections under certain circumstances, especially if you neglect your financial obligations. I hope this guide helps you understand what to watch out for and how to protect yourself from the negative impact of collections related to auto insurance.

Find out more information about “auto insurance send you to collections”

Search for more resources and information: